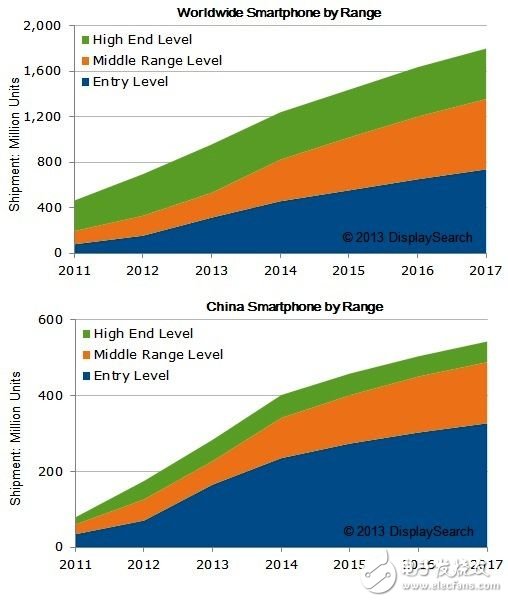

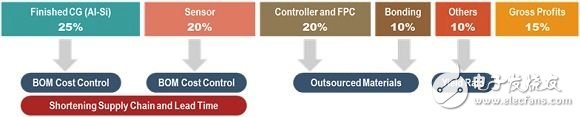

NPD DisplaySearch said that with the rapid popularity of smartphones and tablets, the touch industry maintained a rapid development in 2013; the agency estimates that the overall touch industry shipments in 2013 will reach nearly 31.4 billion US dollars, an annual growth rate Nearly 30%. However, due to the increasingly fierce competition in the touch industry, the touch industry chain has accelerated industrial consolidation. At the same time, some players are also committed to replacing material technology with ITO and laying out the future large-scale touch market. According to NPD DisplaySearch observations, in 2013, especially in the second half of the year, competition in the overall touch industry continued to intensify, and the price of touch modules also declined significantly. Except for the expansion of touch capacity, the evolution of the end market is indeed an important driving factor. Looking back on 2012, the rise of Qianyuan smart phones and 7-inch low-cost tablet PCs has driven the rapid popularization of smart mobile devices and the rapid increase in the scale of shipments of touch modules. With the increasing maturity of the Android system and the rapid improvement of the performance of low-end and mid-range products, the growth momentum of high-end smart mobile devices slowed down in 2013, and the trend of low-cost products is obvious. Taking smart phone products as an example, although the overall market still maintains rapid growth, since the existing products can already meet the daily needs of most consumers, the appeal of simple hardware upgrades to consumers has declined, especially high The high-end smartphone market at a price point is more affected, and growth momentum is slowing. The low-end and low-end smartphone products are expanding rapidly in developing markets such as China and Southeast Asia, becoming an important source of growth momentum for smartphones. Global and Chinese market smartphone shipments (Source: NPD DisplaySearch) NPD DisplaySearch pointed out that due to the impact of terminal product price positioning, the price space of touch modules was further compressed. Referring to the BOM composition of the touch module price, in addition to improving their product technical capabilities to improve the yield rate, the touch industry can integrate the product chain to reduce the production cycle (lead TIme) and reduce the production cost to maintain the existing gains. At the same time, through profitability of products, it can also seek survival space in the increasingly severe industrial competition challenges. In the above situation, the Chinese touch industry has been moving frequently recently, and has carried out industrial integration, adjusted their own physiques, and sought for greater market space, such as: Changxin mergers and acquisitions of Deput, layout of the touch module market; Yuan signed a contract to stabilize the supply of OGS sensors; Oufeiguang raised 4 billion yuan to strengthen the large and medium-sized touch production capacity and entered the display panel module industry; Leybold Hi-Tech introduced Japan Toppan fifth-generation line color film equipment and deployed large-size OGS touch modules Capacity; In addition, Xingxing Technology acquired Shenyue Optoelectronics, Dongshan Precision took over Mudong Technology, United Chemicals acquired Helitai, and BOE officially entered the touch industry. NPD DisplaySearch believes that China's touch industry has begun to enter the scale of competition from the disorderly competition model of low-end products. The market will further concentrate on companies with technological advantages and scale advantages, and some small businesses that are in a disadvantaged position will face elimination Out pressure. Touch module BOM structure (Source: NPD DisplaySearch) As the high-speed growth momentum of the smartphone and tablet market is gradually slowing down, the touch industry is full of expectations for the touch notebook computer (NB) market in 2013, and is actively expanding its large-scale touch capacity. Due to many factors such as the high price of terminal products, the learning cost of Windows 8 and the inventory of the PC industry channel, the penetration rate of Touch NB in ​​2013 was far lower than the optimistic expectations of the PC industry's penetration rate of about 20% at the beginning of the year. To this end, touch-control manufacturer Chen Hong (TPK) has announced plans to stop the operation of the 3.5-generation and 4.5-generation production lines of the Hsinchu plant and delay the installation schedule of the Pingtan 5.5-generation line equipment, with a view to reducing operating costs. situation. However, the touch industry is still actively carrying out industrial layout to prepare for the rise of the large-scale touch field in the future. Among them, SSG (Strengthen Sensor Glass) products led by panel manufacturers and traditional touch companies have layouts of ITO to replace material technology. . NPD DisplaySearch said that due to the consideration of thin products, Apple's tablet computer product series has fully introduced the GF2 architecture of thin film touch technology, and driven thin film touch technology to occupy an advantage in the mobile phone and tablet market. However, due to the influence of the physical characteristics of the ITO film itself, the surface resistance of the film-type touch technology is relatively high, and it will face great challenges when applied to the field of large-size touch; at the same time, the ITO circuit is relatively fragile and the large-size film-type touch Control products are also prone to broken ITO lines during the process, and product yields are facing challenges. Therefore, the traditional thin film-based touch industry is actively deploying ITO replacement materials in order to make up for its deficiencies in large-scale touch applications. In addition, the use of new replacement materials can also reduce the cost price of materials such as metal indium, and at the same time, through coating (coaTIng), gravure printing (Gravure prinTIng) and other process technologies to reduce equipment investment, improve raw material utilization, and reduce costs. Current mainstream ITO replacement material technologies include Metal Mesh, Silver Nanowire, Organic Conductive Material (PEDOT: PSS), Carbon Nanotube and Graphene, of which the short-term In addition, Metal Mesh and Silver Nanowire technologies are more feasible for mass production, which has been studied and adopted by most touch manufacturers. For example, Ophelia uses Silver Mesh-based Metal Mesh process to make thin-film touch products, and actively promotes products on the PC brand side. Verify the import. Nlw-Ecl Pm Fiber,Diode Pumped Lasers,Gemini Diode Laser,Gp Fast Diode Laser AcePhotonics Co.,Ltd. , https://www.cgphotonics.com